Affirm S-1 analysis: Is it a buy?

I reviewed Affirm's recent S-1 filing to dig deeper into their product, business model, and growth. Is Affirm a buy at the IPO?

Affirm is a point of sale lender for online retailers. The company’s mission is to “Deliver honest financial products that improve lives.”

Affirm was started in 2012 by Max Levchin, Nathan Gettings, Jeffrey Kaditz, and Alex Rampell (some joined later as co-founders.)

Product:

Affirm’s main product is an unsecured personal loan from $50 to $17,500 with interest rates from 0% to 30%. The most common loan terms are 6, 12, 24 months but can be up to 48 months in some cases. There are no late fees or any other fees.

Affirm has built APIs to offer instant loans at checkout. If users choose Affirm, they fill out a form, agree to a soft credit pull, and get an instant decision. The loan is paid directly to the merchant and the users repay Affirm over time. As the merchant is paid instantly, 100% credit risk is taken by Affirm. If the user defaults, Affirm loses money but the merchant is not impacted.

Affirm payment option is integrated with 6,500+ retailers.

Originating Bank:

The loans are originated by Cross River Bank and Affirm buys back loans after a short holding period. CRB is chartered in NJ which has a usury cap of 30%. So, maximum APR charged by Affirm is also capped at 30%. Affirm has also recently partnered with Celtic bank (based in Utah) but hasn’t originated any material volume through them. With Celtic, Affirm can charge up to 36% APR.

High level numbers:

6.2M unique consumers since inception

6,500+ merchants

$10.7B GMV since 2017 ($4.6B in 2020)

64% of purchases (or dollars) from existing customers in 2020

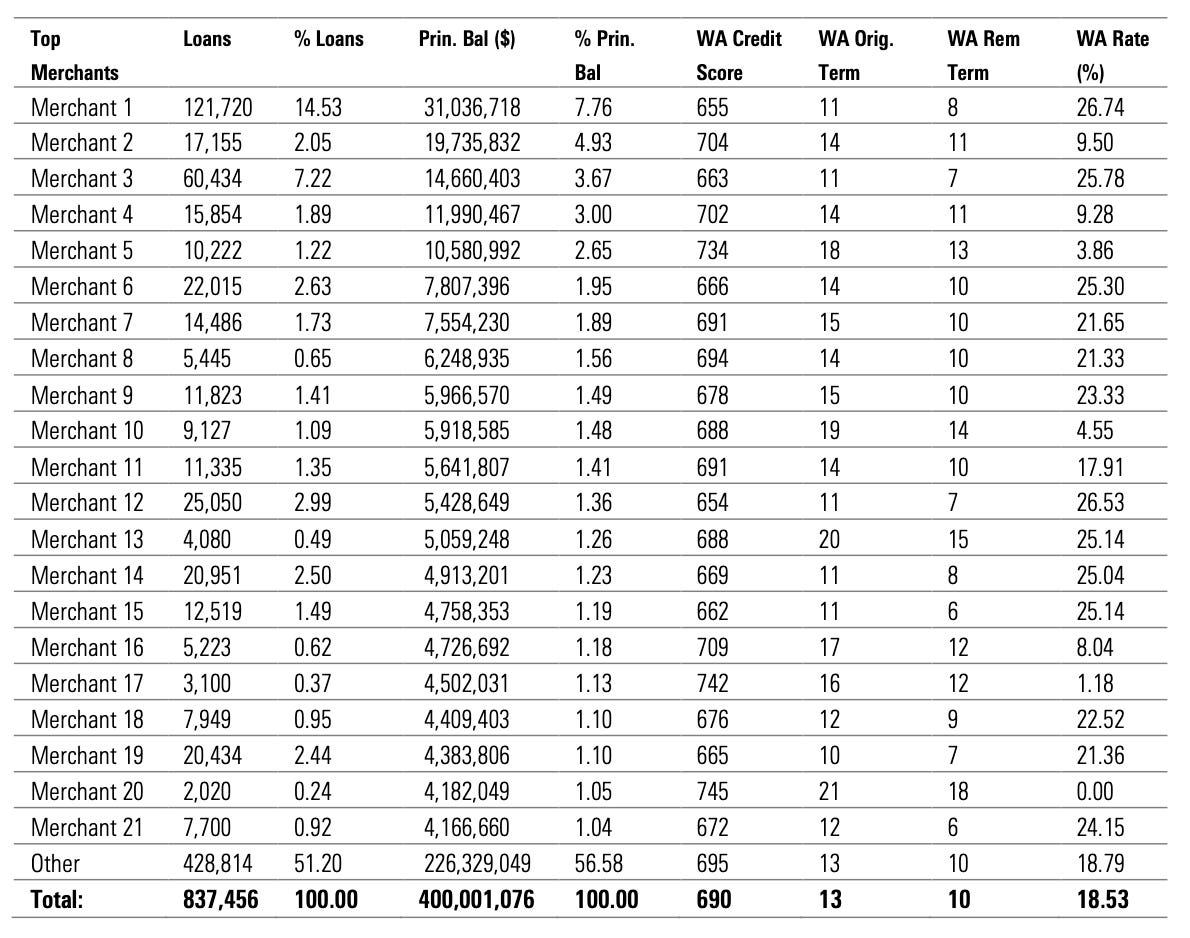

Even though Affirm didn’t mention much about their loan portfolio, we will use their recent and only securitization for analysis. I wrote about it in detail here and will highlight relevant data and some new insights (to help understand the company's revenue and future growth.)

Affirm is posing itself as a replacement for credit cards claiming that legacy financial products are dishonest and predicated on taking advantage of the customer. Compared to these legacy options, Affirm charges only simple interest doesn’t which is disclosed upfront and doesn’t compound interest or charge any late fee.

There’s a quintessential flywheel slide in every S-1 filing. Affirm also has one. I agree with the flywheel but I don’t think it’s infinitely scalable. After a point (which will reach soon), this flywheel will have diminishing returns. The market expansion because of this flywheel is a stretch (for me.)

Affirm’s business model and growth opportunity:

We will analyze Affirm’s business model to identify growth levers and potential opportunities over the next 5-10 years. And we will dig deep here. This is complex and important.

To understand Affirm’s growth potential, we’ll look at their loan portfolio, merchant concentration, and some other metrics.

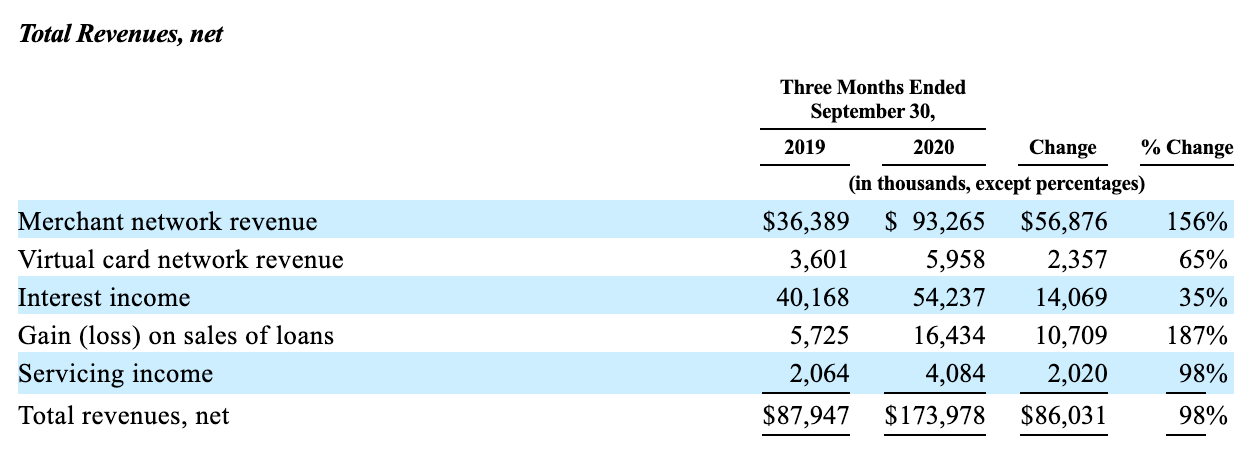

Let’s start with the basics. Affirm has 2 main sources of revenues:

Interest charged from consumers

Fee charged from merchants

The other sources are Virtual Card Network Fee, Servicing Fee, and Gain/Loss on loan sales.

Interest Revenue:

For this discussion, we will assume that Affirm’s securitized loan book is representative of their overall loan portfolio. We will also discuss differences in some cases.

Based on Affirm’s securitization, their average APR is 18.53% excluding their biggest merchant - Peloton (30% by GMV). If we include Peloton, I think the average interest rate will be way lower - my best guess is 15%. The average term of the loan is 13 months (ex. Peloton) and cumulative net losses are 2.5% - 4.5%.

Another interesting point - in the securitization report, 26% of the loans had 0% APR but S-1 filing says overall 0% APR share is 46% (as of Sep 2020). My guess - most of the remaining 0% APR loans are for Peloton (which were excluded from securitization).

What we don’t know:

Affirm doesn’t provide details on average interest rate by month since inception. So, we don’t know how the average interest rate is changing over time. Based on revenue numbers, average interest rate seems to be going down. Yes, the default rate is also going down but we need both to determine Affirm’s interest rate spread.

We know GMV is increasing but we don’t have any insight into key portfolio metrics. e.g. average loan amount and average interest rate by cohort.

Affirm hasn’t shared these numbers on purpose. I think, now they offer big loans at 0% APR to high quality customers and their primary revenue source is merchant fees. Their average loan amount for non-interest bearing loans (0% APR) is $1,153 compared to $680 for interest bearing loans.

Here’s how I think the portfolio composition is changing:

The average loan amount is increasing - we know that the average loan amount was $250 and now increased to $477 (ex. Peloton) and probably ~$750 (including Peloton)

The average interest rate is decreasing - 18.53% (ex. Peloton) and probably 15% (including Peloton)

The average loan term is increasing - larger loans have longer loan terms

If we extrapolate this, the share of merchant revenue will continue to increase compared to interest revenue.

We also see this reflected in their revenue distribution. Interest income reduced to 31% of their total revenue for three months ended in Sep 2020 (compared to 47% for three months ended in Sep 2018).

This may be concerning because it shows that Affirm can’t grow without lowering interest rates and we don’t know if merchant fee revenue will be enough to make up for it.

Merchant Revenue:

Affirm charges merchants a percent of GMV when a customer finances a purchase using Affirm. Affirm deducts this fee from the proceeds sent to the merchant. This fee is a 100% gross margin revenue and I expect it will be the main source of revenue for Affirm in the future.

Also, for all merchants with 0% APR financing option, Affirm must be charging a higher merchant fee because that’s the only revenue source to pay for loan defaults.

Affirm processed $4.6B in GMV and earned $256M in Merchant Network Revenue - which translates to 5.56% of GMV for Fiscal year ended on June 30, 2020. It is 36 bps higher than June 2019 (5.20% of GMV).

I think Affirm has leverage with merchants. Once merchants are addicted to increased revenue because of Affirm, they will pay more to continue that growth. Affirm may even charge a higher fee to increase approval rates. The upper limit on this fee depends on a merchant’s gross margins.

But there’s also merchant concentration risk. We will touch on it a little bit later.

Other Revenue sources:

Virtual Card Network Revenue: Affirm also offers virtual cards to shop at retailers where Affirm is not integrated. When customers use this virtual card, Affirm earns interchange revenue. This product hasn’t really taken off since its launch a few years ago. It contributes 3%-4% of overall revenue in any given quarter since 2018.

Servicing Fee Revenue: This is a standard 2% fee earned by Affirm on outstanding principal balance (based on securitization report).

Gain (loss) on loan sales: This revenue fluctuates depending on the expected performance of the loans, how seasoned they are, and the carrying value. It shouldn’t be considered a material revenue for business analysis.

YoY growth in revenue by category:

Merchant Concentration risk:

Peloton contributes 30% to Affirm’s GMV. This is a big merchant for them and such a high level of concentration is not good. But it’s not just Peloton, Affirm’s 2nd highest merchant is 7.75% of GMV, and 3rd highest is 4.93%. Based on their securitization report and Peloton, the top 5 merchants contribute ~50% of their overall GMV. Affirm needs to diversify this risk as quickly as possible. That brings us to their growth strategy.

Growth Strategy:

Affirm has a few growth levers but they are primarily dependent on merchant acquisition. If they can acquire merchants at a rapid pace, they can grow revenues faster. That’s why Affirm is super-changing its growth strategy. Instead of directly going to merchants, Affirm is partnering with large platforms that serve online businesses. This path is so important that they gave away 5% of the company for a 3-year exclusive contract with Shopify. In addition to that, Shopify will earn a fee for every loan originated for merchants on their platform. But Shopify will integrate exclusively with Affirm for 1,000,000+ merchants. They couldn’t have managed the same reach on their own even in 5 years. I’m sure Affirm will partner with more platforms and payment processors in the future.

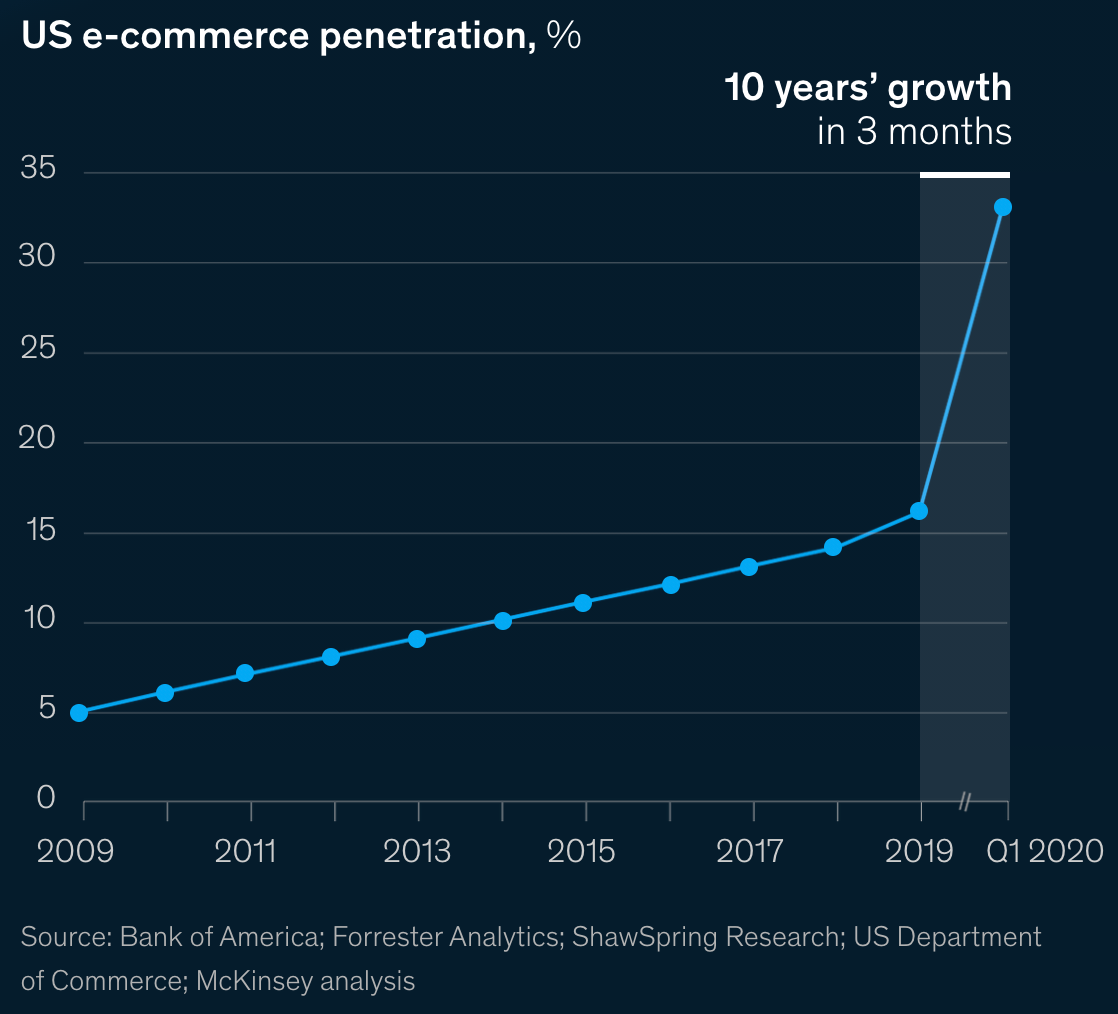

Affirm has strong macroeconomic tailwinds. E-commerce penetration has jumped to 30%+ in 2020 (after the COVID-19 pandemic). As big purchases happen online, they increase Affirm’s TAM and this trend is not slowing down.

Other levers for revenue growth:

Average loan amount - Affirm will try to increase average loan amount to show a fast growing GMV but I think a large part of this will come from 0% APR financing.

Average interest rate - Affirm can charge higher rates for riskier FICO cohorts but that’ll increase the overall risk of the portfolio. I think they will offer big loans at low rates to increase GMV and reduce dependency on interest.

Merchant Fee - a higher merchant fee will increase revenue. But it is limited by competition and how much merchants are willing to pay for growth.

Offline Merchants - Affirm doesn’t have a strong presence in the offline world but with omnichannel retail becoming the norm, Affirm can sign up big offline merchants (in addition to purely online merchants.)

New markets - Affirm is currently primarily in the US and have resources to go international. But the US will be the biggest market in the near future.

Merchant and Customer Retention:

Affirm has also shown good merchant retention. On average, Affirm is originating 2x loans for merchants in 3-4 years. It would be interesting to see what % of a merchant’s overall revenue is funded by Affirm. If that number is also increasing, it’s a win-win.

Affirm has 3.9M active customers as of Sep 2020 (who used Affirm to make a purchase in the last 12 months), growth of 65% YoY. It is encouraging to see that these customers are increasing their purchase frequency. They are using Affirm 2.2 times over a 12 month period. But overall, it’s still a low number. We don’t know the growth of customer purchase frequency by cohort. I think Affirm will try hard to increase purchase frequency (also mentioned as a part of their flywheel).

Given Affirm has had 6.2M customers since inception, 37% of them haven’t transacted with Affirm in the last 12 months. I haven’t seen benchmark retention rates .

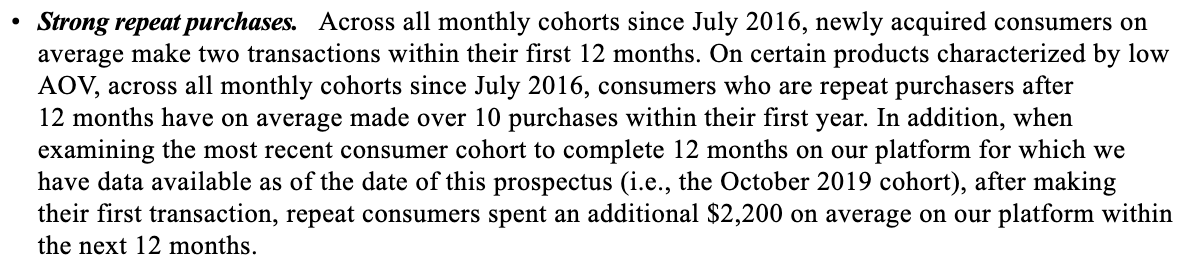

But this paragraph from management is interesting:

Customers that make low AOV purchases are making 10 purchases per year.

Repeat purchasers spend an additional $2,200 after their first purchase in 12 months.

Competition:

Affirm is right in the middle of a super competitive environment with payment processors, buy now pay later (BNPL) companies, credit card companies offering payment plans, and behemoths like Paypal offering their own services.

Afterpay and Klarna are rapidly expanding their merchant network. Paypal offers Paypal Credit (Pay in 4). Affirm knows that Stripe will eventually offer loans to end customers, Square has already done it with Square Installments. Goldman Sachs is partnering with big retailers like Amazon and JetBlue. All of them are coming for Affirm’s market. New smaller players are also coming up.

Affirm has no real moat in this market. If another player is willing to take more losses with their balance sheet, they can replace Affirm as the point of sale lender. Many merchants may add all BNPL or POS loan options.

Biggest Risks:

Lack of success of new products - I think Affirm will face the product expansion conundrum beyond their core loan product (and BNPL option). They have recently re-launched their checking account but I don’t see it being successful the way their POS loans have been. The Virtual Card product is still contributing only 3% of revenue for the last 3+ years.

No real moat - Affirm touts its underwriting model (which is good) as the key differentiator but underwriting gets copied over time. As other players lend, they also build models on billions of data points and millions of loans. The extra lift in conversions and approval rates become similar for all merchants.

Pricing power - I am concerned that Affirm doesn’t “own the end customer” and has no real pricing power. Their loan portfolio will generate lower revenue over time (as a percentage of GMV). But merchant fee revenue will increase (with an upper limit that we don’t know yet).

Management Team:

The executive team is top-notch.

Max Levchin is the CEO. He’s a tech industry veteran and a legend in his own right. He co-founded Paypal and was the CTO until its sale to eBay.

The rest of the management team has extensive experience in technology, finance, and capital markets. Nothing special to note here.

Things I didn’t discuss:

Default rates: It is crucial for a lending company to manage defaults but I don’t think Affirm will run into poor credit quality problems. They have probably one of the best data science teams and they will manage credit well.

Cost of capital: Another important aspect is “cost of funds.” Because of low Fed funds rate, Affirm’s cost of capital is low and I don’t think the rates will increase anytime soon. Even as they increase, Affirm can accordingly charge higher rates.

Future products: I don’t see a clear product roadmap from Affirm for the next 2-3 years. Even if they launch new products, I don’t expect these products to materially contribute to revenue for a while. So, we have to assume that the majority of the revenue will still only come from the POS loan product.

Summary:

Affirm is definitely interesting and I find their approach to increasing market share intriguing. I have no doubt that they will show rapid GMV growth for the next 3 years. But I am not sure about any operational leverage in their business model. It’s going to be a constant battle for margins. The only way Affirm can win is through big merchant partnerships with long lock-in periods or dependency on their loans. There’s a risk of merchant concentration through Shopify and Adyen.

We will have to see how the market values Affirm. Afterpay (a BNPL player) is currently valued at 54 times LTM revenue with a market cap of $27B. This is a rich multiple. Affirm is valuing itself at a similar level - $250M (revenue) X 40 = $10B. Both companies earn 5%-6% of GMV as revenue and are growing 90% YoY.

Affirm can be interesting at the right valuation. I may buy Affirm at IPO to keep a close eye on it. If I see any signs of operational leverage, stable/increasing portfolio interest rates (including merchant fee), or big merchants preferring Affirm over other providers, I may start a position. I will also like to see Affirm contributing a higher % of a merchant’s overall sales.

Hope this is helpful in understanding Affirm.

I am always around for discussions. Feel free to follow me or send me a note on twitter @rohitdotmittal.

Please subscribe if you liked it and would like to receive future essays.