Analyzing Affirm's $400M Asset Securitization

Affirm, an online point of sale lender, completed its first securitization. Below, I'll share what I've learned. In the end, I'll also discuss key metrics that should have been in the filing.

Company:

Affirm is an online point of sale lender. It integrates with online retailers and offers unsecured personal loans at the time of purchase. Affirm was started in 2012 by Max Levchin, Nathan Gettings, Jeffrey Kaditz, and Alex Rampell (some joined later as co-founders.) It has grown to be one of the biggest online lenders. The company has raised $900M in equity and was valued $3B in its last funding round. Affirm partners with 4,000+ merchants, has originated 15.1M loans with a total of $10B origination volume.

Loan Product:

Affirm’s flagship product is an unsecured personal loan of up to $17,500 with interest rates from 0% - 30% and loan terms from 1 month - 30 months. The loans are close end, fully amortizing, fixed and simple interest, with no prepayment penalty. Also, there are no late fees.

Securitization:

On June 26, 2020, Affirm announced securitization of $400M in outstanding principal balance. It excluded all loans greater than 24 months in the transaction. The loans were originated using a rent-a-charter model and Cross River Bank (New Jersey) is the originating bank. The securitization will have an 18-month revolving period - that means Affirm will replenish the portfolio with new loans as existing loans are paid down. The refill will be subject to concentration limits and eligibility criteria.

Portfolio:

Total # of loans: 837,456

Principal Balance: $400M

Average Interest Rate: 18.53%

Weighted Average Original Term: 13 months

Cumulative Net Losses: 2.5% - 4.5% (based on static pool analysis)

This is an interesting portfolio with a small loan size ($477.63) and a short payback period (~1 year). Because the loans are fully amortizing, investors will get 50% of the principal back in just 6 months.

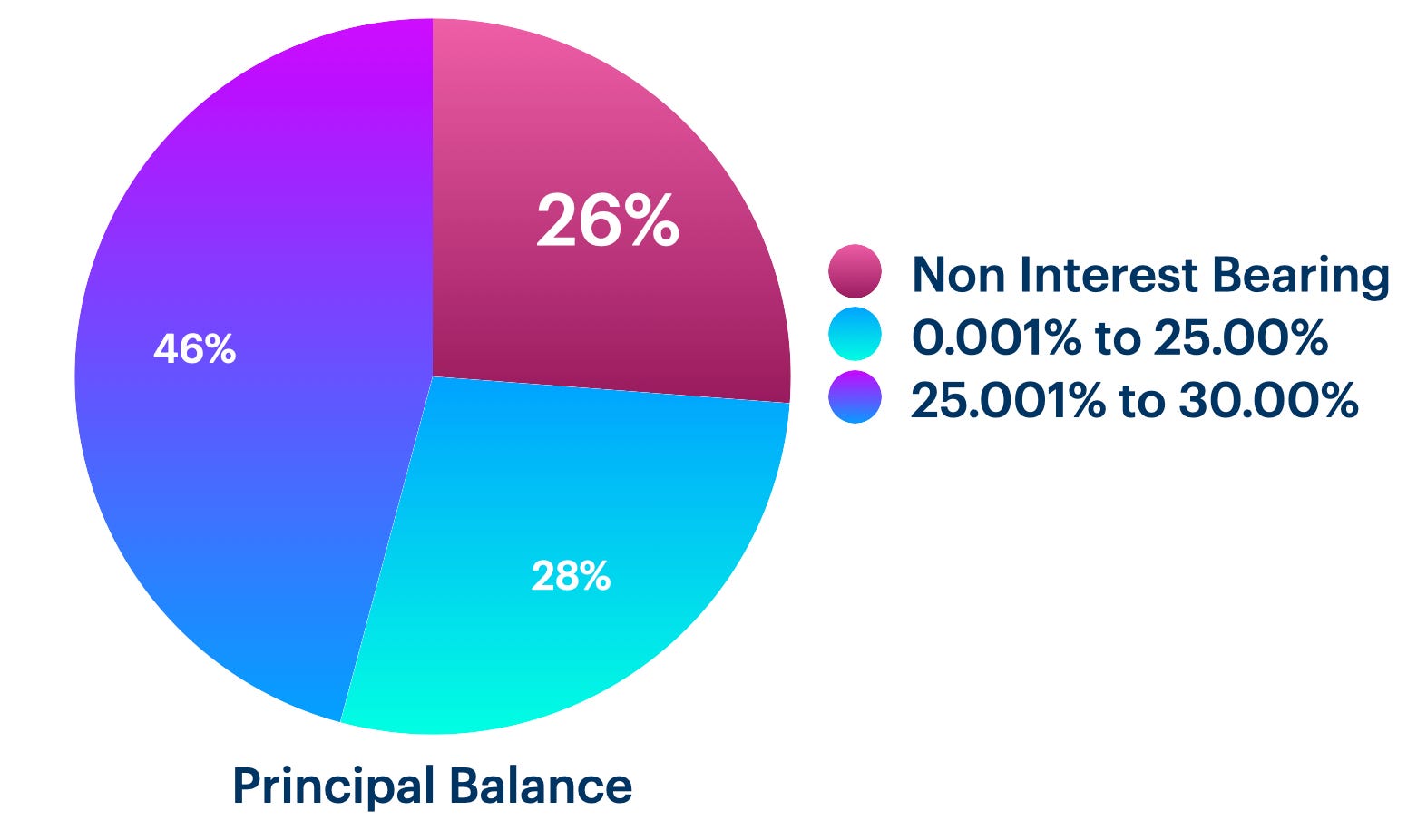

~26% of the loans are non-interest bearing. This means that merchants are offering 0% interest rate financing options. These merchants are selling big-ticket items to high-end consumers (which is reflected in bigger loan amounts.)

The average loan size for interest free loans is ~70% higher than interest bearing loans.

The average rate on interest-bearing loans is 25%, which is close to high-interest rate credit cards. So Affirm is not cheap for borrowers.

Loan Amount:

Affirm offers up to $17.5k but most loans are below $1,500. Most customers would not want to borrow large amounts for impulse (or non-urgent) purchases. It is interesting to see that the Weighted Average Loan Term increases from 12 months to 15 months while WA Interest Rate decreases from 23% to 14% for larger loan amounts.

It seems like Affirm lends interest-free loans across all loan size but I expect that most of those loans are in the higher loan amount bucket.

*$2,000+ - WA Interest Rate is approximated for clarity

Repayment period:

Affirm’s average loan payment term is 13 months. A shorter repayment period is both good and bad. It’s good because of a higher certainty of getting money back and bad because Affirm has to constantly replenish the portfolio. It’s bad because replacing loans in a portfolio comes with its own risks. There are risks of new merchants that bring in lower credit quality loans. The overall portfolio risk may change from the original portfolio even if concentration limits are satisfied.

The average loan size for 3-month loans is $302 and increases to $1,302 for 24-month loans. Affirm doesn’t increase loan amounts proportionally to loan term because higher monthly payments could be problematic with long repayment terms.

75%+ of the loans have an original loan term of 12 months or shorter.

The interest rate decreases as the term increases, which makes sense. But note that 12-month loans are charged the highest interest rate and also have the biggest concentration in the portfolio. Affirm is pushing those loans for better unit economics.

FICO distribution:

Even though Affirm claims to be built for people without credit scores, they are a negligible portion of the overall portfolio. Only 0.09% of the loans are given to customers without a FICO score.

Affirm targets mostly non-prime customer segments for these loans. But the average interest rates are higher than sub-prime credit cards. The customers paying these high rates are either finding it valuable to borrow at the time of sale or they don’t have other options. Still, the high rates allow for a larger margin of safety.

72% of the loans are to customers with FICO scores between 600-699.

As Affirm signs up new merchants (who were not included in the original transaction), the credit quality of loans from those merchants and categories of loans may be different.

Let’s look at each of these more closely:

Merchants:

4,000+ merchants use Affirm as a point of sale lender. Merchant names are not disclosed in the transaction but Affirm’s website lists some big names like Peloton, Casper, Expedia, and Dyson. These websites mostly sell premium products.

Top 10 merchants account for ~30% of the volume while the top 21 account for 43.42%.

The weighted-average credit score at most large merchants is below 700.

The top 10 merchants contribute 30% of the loan volume.

A potential risk of changing credit quality:

If any of these merchants stop using Affirm, they’ll have to refill loans with smaller merchants and the quality of loan through those merchants may be different. Affirm is required to maintain concentration limits (in terms of credit risk) but the risk of the underlying borrower is different based on the merchant.

Here’s an example:

We clearly see that Merchant 10 has a lower average FICO but Affirm charges only 4.55% interest rate. Affirm may have different risk grades that don’t match FICO scores but this is not a good look for debt buyers. It is possible that Affirm gets a kickback from the merchant to drive sales and Affirm subsidizes the rates for that merchant.

We also don’t know the type of product these merchants sell. There is variability in credit quality by product category but we have no insights into that.

Also worth noting that Affirm has recently signed deals with large merchants such as Walmart and Shopify. Affirm may include loans originated at these merchants in the portfolio but the credit quality may be significantly different.

Merchant Type:

Affirm offers loans across 23 categories including “Other” as one of the categories. Interestingly, only the top 3 categories contribute 50%+ of the loan volume.

The “Furniture/Homewares” has the largest principal balance but weighted average interest rate is one of the lowest. It raises questions on how many loans in this category are non-interest bearing. As we saw with merchants in the earlier section, Affirm maybe using kickbacks from merchants to justify lower rates for customers.

Online DTC mattress providers have exploded in the last few years and it’s possible that all the mattress companies are a part of that category. Affirm may be incentivized to increase sales for these companies.

As e-commerce is growing, Affirm will grow with merchants. New partnerships with companies like Walmart and Shopify will help Affirm scale faster. But again, the credit quality of customers through these platforms is unknown at this point.

Defaults/Losses:

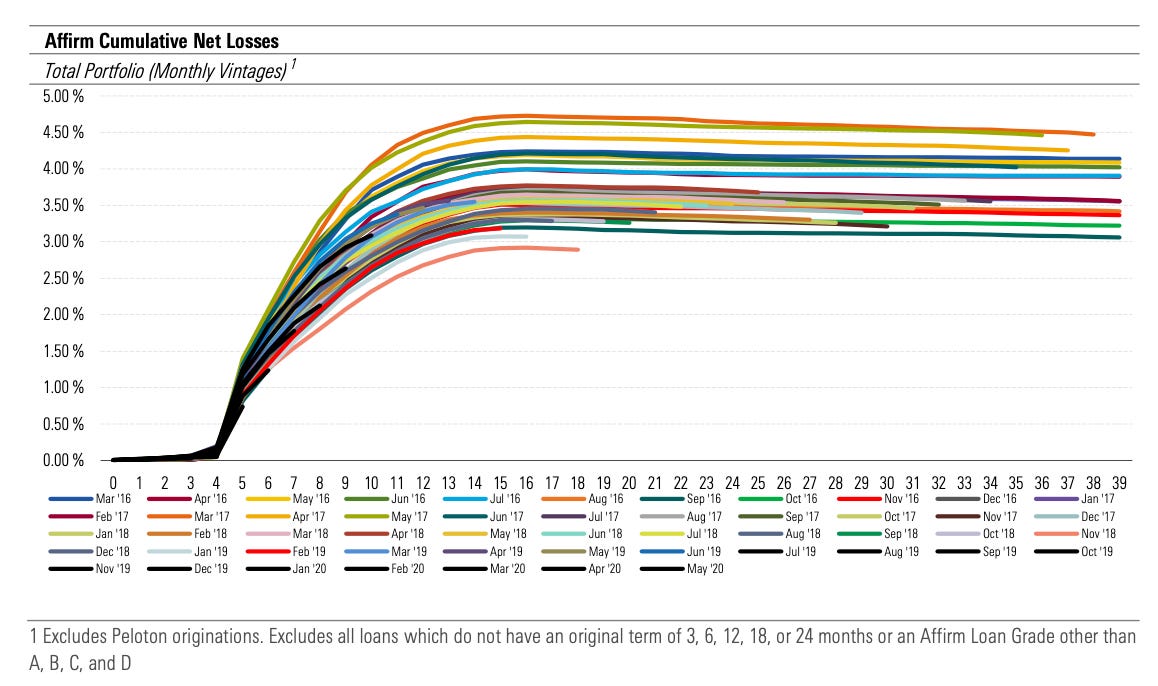

Affirm has maintained a fairly good loss rate given the customer base. Compared to securitizations of similar credit quality portfolios, Affirm is 2x-3x better than their peers. This speaks to the acquisition and underwriting strengths.

We also see that Cumulative net losses decrease after 24 months or so. This means that Affirm is able to recover some principal many months after the loan term is complete. But we don’t know if Affirm makes money net of collection costs (cost of collections are unknown).

Cumulative net losses range between 3.0% - 4.5%

Servicing Fee:

A 2% fee seems high for a portfolio that can be serviced completely digitally. I don’t expect that Affirm is collecting payments in physical checks or through in-person kiosks. If the payments are managed online, the cost of servicing is expensive.

Affirm doesn’t charge a late fee, so maybe they are trying to make up for that revenue. The only other possibility is that Affirm needs a large customer support staff for collecting payments (that may justify a higher servicing fee.)

Missing Data:

I was surprised by the amount of missing information from the securitization report. I don’t expect this data to be shared in the future. The missing data makes me pause about the future quality of the portfolio.

Below are some key data I would have liked to see:

Borrower Income: No mention of the average income of borrowers. A higher average income is a good sign. Also important to understand trends in average income as Affirm scales originations with new merchants.

Existing vs Repeat Borrowers: There is little to no information on new vs repeat borrowers. We don’t know how many borrowers take two or more loans and what % of the book is repeat loans. We also don’t know what % of borrowers have multiple active loans. A repeat customer could be a good sign but multiple loans per borrower could be potentially negative.

Delinquency: Affirm only shared cumulative net losses but did not share 30 DPD and 60 DPD analysis. Early delinquency numbers help investors understand the portfolio quality better and also impacts the base for servicing costs. For e.g. if the roll rate from 60 DPD to 90 DPD is high, investors will not want to pay for servicing after a loan is 60 days delinquent.

Origination Growth: Affirm wants to keep growth metrics close to its chest (at least before the IPO.) But it is important for debt investors to evaluate loan performance with growing origination volumes. Generally, lenders tend to loosen up credit criteria as they grow originations and if that’s the case, investors will want to be paid for higher risk.

Prepayment Rates: Affirm doesn’t charge any prepayment fee and I’m assuming some borrowers would prepay. A higher prepayment rate has pros and cons. The advantage is that the portfolio is exposed to a lower risk of default but the disadvantage that the portfolio will need to be replenished faster. New loans in the portfolio are prone to the risk of degrading credit quality.

Merchant Fee: Affirm is, obviously, charging merchants a fee for boosting their sales. It is important that Affirm discloses this fee to investors otherwise it leads to misaligned incentives. e.g. Affirm may choose to lower credit quality for some merchants to increase originations, charge lower rates, and earn a fee directly from the merchants (which is not paid to debt investors).

Affirm’s portfolio is performing fairly well to attract debt investors. It is also less likely to blow up due to factors like COVID because the loan amounts are small and loan terms are short. Affirm can quickly tighten the credit criteria if the performance starts to degrade.

Thanks for reading. I’d love to hear your thoughts or if you want to better understand or just discuss. I love this stuff and can do this all day long.

If you liked what I wrote, please consider subscribing. It’s free. For now.