A brief guide to starting and building a lending business

There are 5 areas in a lending business - product, acquisition, underwriting, debt capital, and compliance. I share how founders can build a business by focusing on the right things.

Starting a lending company is really complex. It’s a lot more complex than building a social app. This is because a lending company has disparate functions such as debt capital and compliance. All these moving pieces need to work in lockstep. Scaling is also harder because of each function’s complexity and uneven speed of execution. For e.g. if you scale acquisition but don’t have debt, you will lose customer trust. But debt capital is tricky, needs equity cushion, and takes 6-9 months to raise. If you don’t manage compliance, it will lead to fines. But compliance slows down product innovation. Successful unique underwriting in the early days can lead to discrimination at scale. So it needs to be reset - which may kill a business model. The list goes on.

When we started Stilt in 2016, we did not know much about building a lending business. In the past few years, we had to learn all the functions from scratch. We read compliance statutes, built payment systems, raised debt capital, and everything else needed to build a lending company.

With the increased interest in fintech, a lot of founders reach out for advice on starting/building a lending company. So I wanted to share my learnings with the hope that it makes their lives a little easier.

Building a lending company has 5 major areas of focus:

Product

Acquisition

Underwriting

Debt capital

Compliance

The interactions and interdependencies between these functions are unique for each lending business and difficult to balance (especially during growth). I am skipping other functions like “Servicing” and “Fraud” for the sake of simplicity.

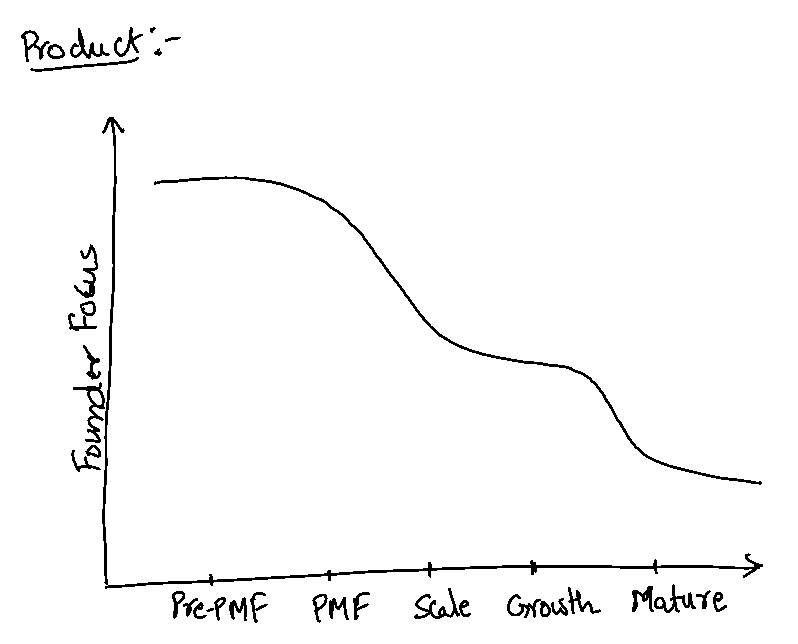

We will look at the importance of each function across different stages: pre product-market fit, post product-market fit, initial scaling, growth, and stable/mature stage.

1. Product

In most cases, a new lending product either provides access to capital or reduces cost. This is the most important area of focus in the pre product-market fit stage. If you haven’t defined a clear value proposition and ideally, tested it with the target market, you should not focus on anything else. It is easy to get distracted. At this stage, focusing too much on compliance, debt, or something else is a waste of time.

For e.g. Affirm - it took about 12 months before they found an online point of sale product. They did not focus on anything else until they found a product that worked.

Online lending is a huge category and has many variations. There are dozens of products with unique parameters. The goal is to find a product that people want and that actually makes money. It’s easy to give away cheap money and consider it a product-market fit.

Common pitfall: Offering negative unit economics product to make it work. Unless the product is really unique with high retention, test a higher potential price to verify customer demand. Many products work at low prices but fail when they are expensive.

Now, after finding product-market fit, you can start allocating time to other functions. Most fintech products stay the same for years, you won’t change it once it starts working.

You continue to drive the product direction but hire PMs to work on the details. You will continue to drive the broad product direction during the growth and scaling stages, but the fundamental product won’t change.

2. Acquisition

Acquisition is extremely important in fintech. This is the hardest (or second hardest) thing for fintech companies. After the initial product-market fit, founders need to focus on how to consistently acquire customers cheaply. The market pulling the product out of you doesn’t work well for most fintech startups. Fintech investors discount any fintech startup without unique acquisition advantages (at least in the early days).

Common problems with acquisition - The early channels won’t work at scale. With new channels, you will start hitting the growth ceiling quickly and the CAC will be through the roof. Marginal CAC on Facebook gets super high. Google CPCs are already expensive. This is because you will start competing with banks, financial institutions, and other lenders. They have bigger brands, deeper relationships, and higher LTVs, so they can spend a ton on marketing.

So you will need to get really good at large channels, be able to change your tactics quickly, and find new channels at least every few months and at the max every year. For e.g. if you are lending, eventually someone’s going to recommend using direct mail, but it is so saturated that you will fail unless you commit to it with a big budget and go deep into the weeds to find your advantage.

Some examples of good acquisition channels include - B2B2C partnerships (Affirm), Referrals (Robinhood), Developers (Stripe).

Acquisition will continue to be one of your key focus areas even as you scale the company.

3. Underwriting

Credit risk is obviously important for fintech startups. But you need to spend less time on this than you think. Your focus should be on finding new data sources for underwriting. And the time spent here should be directly proportional to how unique the data sources are. For e.g. if you are serving a previously underserved population, you need to focus on alternative data (preferably that no one else has or will have). But if you are using credit bureau data for underwriting, don’t spend a lot of time here.

With alternative data sources, founders should make sure that they are non-discriminatory, reliable, consistent, and have a high coverage to build risk models. After that (and product-market fit), hire a Head of Credit Risk, and let them own it. Don’t overoptimize on risk models without a product-market fit. Also, note that credit risk models are iterative and improve quickly as you lend and get repayments.

All big lending companies started with simple (and non-quantitive) risk models. e.g. SoFi primarily used university, income, cash flows, and FICO; Lending Club used simple regression models on credit reports.

Your risk models help you manage risk but the goal at this step is to make sure you can make money profitably. The interest rate charged should cover the cost of debt, absorb expected defaults, and still leave money to run the business (including acquiring customers).

The biggest risk with underwriting is at the growth stage. This is because of 2 reasons:

Overall risk quality of applicants change quickly - In the early days, you know your customers and credit risk well. But as you grow, the quality of consumers or businesses applying for credit will change considerably and after a point, the law of large numbers will take over.

Untested models on large population - Your models are not tested on a large userbase and as the risk changes, models need to be constantly retested, and calibrated else defaults will increase massively.

*I’m not going to cover Servicing in detail here but is the other side of underwriting that comes into play after a loan is disbursed. It is also operationally intensive. Building a good servicing function takes time and it can be 50% of your total team. It is also important to debt investors.

Focus on building an iterative setup and make sure models are compatible with debt capital requirements and compliance.

4. Debt Capital

A lending company’s core product is “Money.” And debt capital funds the core product. Raising debt is the founder’s primary full-time job after the PMF stage until growth stage. In the early days, companies can fund loans with equity but that runs out when you start to scale. Using equity is sometimes necessary but you don’t want your equity stuck in loans.

Raising debt has long timelines (longer than you’d expect) and it’s expensive. Getting your first line will be the toughest. You can’t run a time-bound process (common for equity fundraise). A debt deal will take anywhere from 6 months to 18 months and costs $150k+ in upfront legal expenses.

Founders need to lead debt fundraise at 2 stages, getting the first small line, then the first big line. For both of these lines, debt investors will take a bet on you as much as they evaluate the data. After you have enough performance data and equity capital cushion, you can hire a Head of Capital Markets to scale the function.

A counterintuitive approach with debt capital is to not worry about the cost of capital until your Series B/C. It is easier to raise expensive debt compared to cheap debt. Expensive debt providers need limited performance data and they close faster with lower legal costs.

It’s also easier to raise debt capital if your loan amounts are smaller and get paid back faster. e.g. raising debt for a new mortgage product is more tricky than raising debt for a “$1k loan for 12-month” product.

*I wrote a post on raising debt from seed to ~Series C - Lessons in raising debt capital

There will always be the next big line at a lower cost. And it will still take up your time but it won’t be your primary focus.

5. Compliance

How much time should a founder spend on compliance always leads to debate. Generally, technical founders are not well versed in compliance and don’t know where to start. So they talk to the best lawyers, try to acquire licenses, and build this function prematurely because it makes them feel like a growing startup. This is something founders need to actively avoid (unless you are selling to banks or other regulated clients). Try to figure out how you can launch without any licenses. Most B2C startups should be able to figure out a way to operate with limited or zero compliance requirements. B2B compliance requirements can be significantly different from B2C startups.

*I’m not discounting the importance of compliance. Just when to focus on it. Some B2B startups do need compliance to launch. e.g. BaaS (Banking as a Service) startups, Cloud Lending Technology providers.

It is difficult to fully comply with all the regulations in the early stages and founders shouldn’t try to. Before you find product-market fit and solidify a final product version, don’t worry too much about compliance. You’ll need compliance at the growth stage because you won’t be able to scale without it.

After Series A/B, you can set up a compliance team and let them drive it. Compliance slows down product innovation and iteration but necessary for a long-term sustainable business.

Here’s a graph to visualize the relative importance of all five areas:

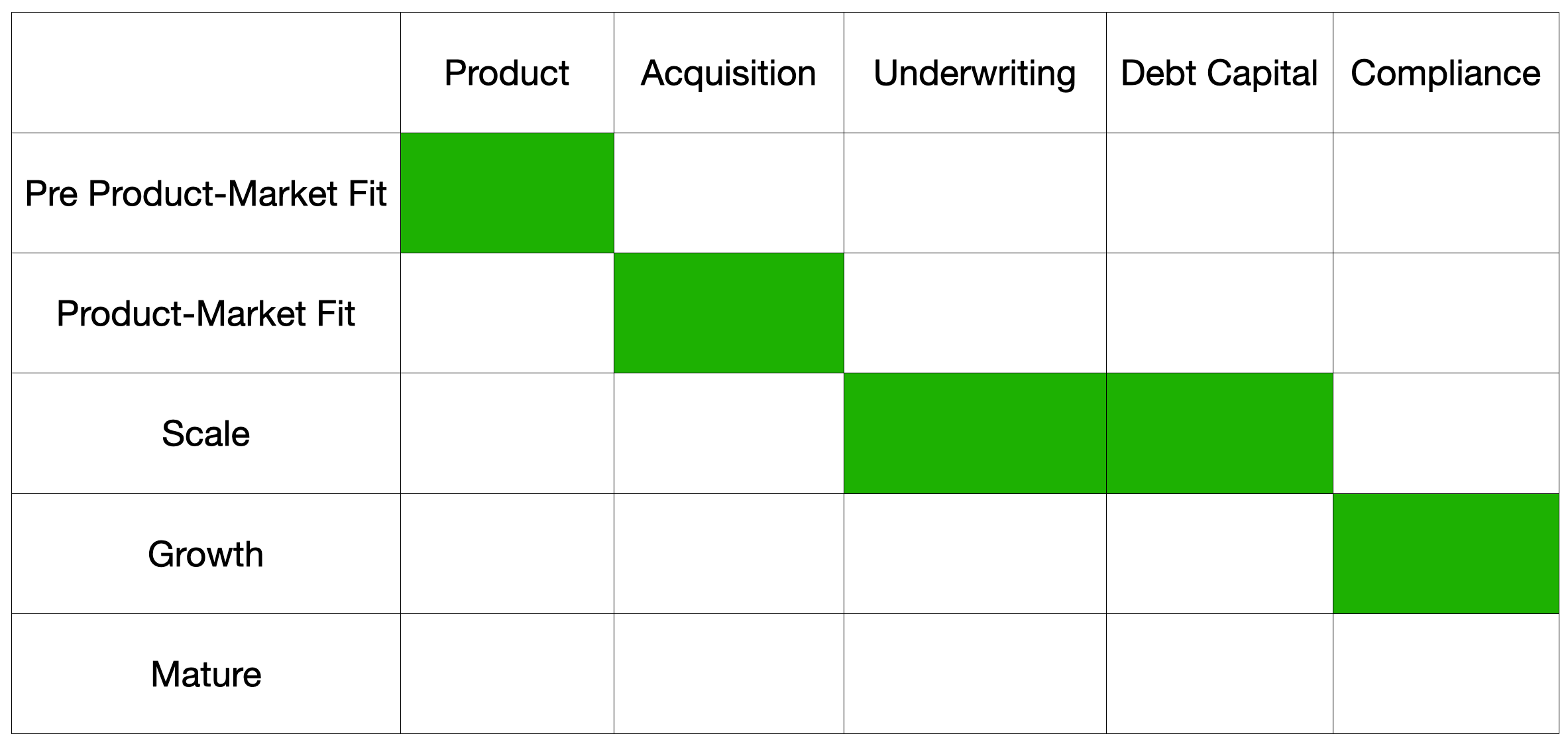

The chart above is shown as a discrete matrix below. The green cells indicate the most important function at each stage.

Final note: Building a fintech startup is not a linear process. You’ll iterate throughout as you find product-market fit, test acquisition channels, scale, and grow into a multi billion dollar company. The things you’ll iterate on will change as you grow.

Hope this is helpful to new founders when building a fintech startup.

I wouldn’t have learned without help from a lot of people.

I am always around to help if you need any feedback or advice. Feel free to follow me or send me a note on twitter @rohitdotmittal.

Please subscribe if you liked it and would like to receive future essays.

Rather than closing the first line of debt facility, how about partnering with a large retail or corporate bank, to basically originate loan for them up to a certain amount, but taking none of the risk. A lead origination play basically (unsure if this would require a formal forward flow arrangement necessitating external lawyers and a $100k price tag - or if this is standard for some retail banks) until you get a solid track record to go an raise the debt?

This was pretty good :)