Access vs Cost

How should credit/lending companies think about innovation?

Fintech startups have been slowly taking customers away from banks — one product at a time. These startups are also eating profitable business lines for banks. As startups scale with a unique product wedge, they have started offering new products to their large customer base. Even large tech companies are jumping into the pool with financial products for their massive user base. All of this has made fintech a hot industry in the last couple of years.

There are a lot of categories for consumer fintech startups including but not limited to credit, neo-banks, p2p payments, real estate, and remittance. In all cases, the value proposition of most startups is either:

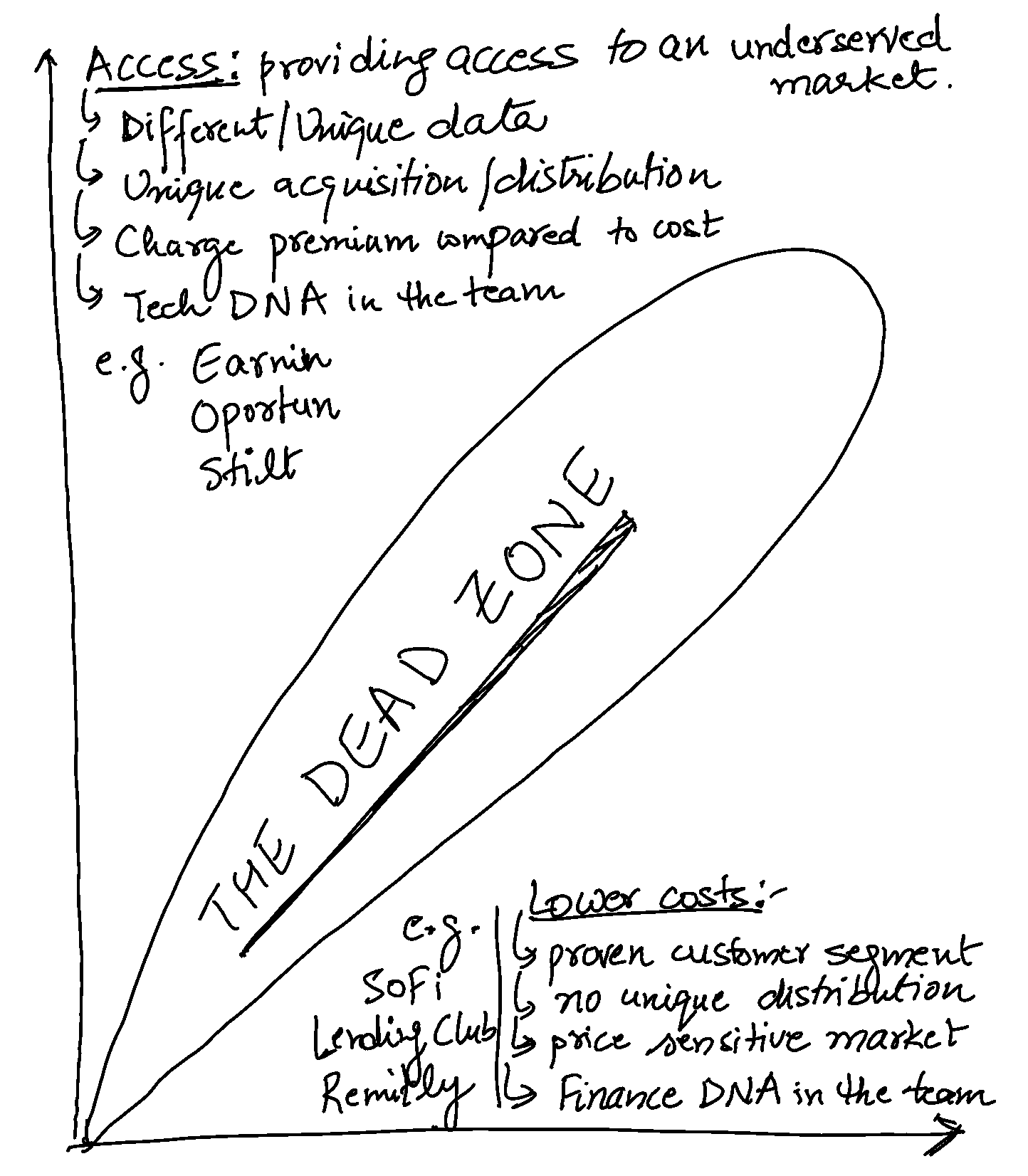

Lowering Cost — e.g. Lending Club, SoFi, Chime, Remitly

Increasing access — e.g. Oportun, ZeroDown, Earnin, Stilt

Improving the experience — e.g. Flyhomes, Wealthfront

Improving transaction speed — e.g. Klarna, Opendoor

All startups touch on these 4 things in some capacity but only one of these areas is core to their value proposition. It is important to choose a focus area upfront (or at least to identify it). This is really helpful in knowing where you add value and 10x-ing the right value proposition for your market. This focus is independent of your product. There are very few companies that create completely new products (in how they work) that haven’t been seen in the industry. Because financial services is largely a commoditized industry with intense competition, you will be irrelevant and die quickly without a clear focus (generally true for all startups).

If we look at credit/lending startups, all of them fall in 2 main buckets — either they lower costs or improve access for customers. It is crucial for startups to focus on one of these value propositions and try to 10x that. If your product tries to do both, it will be difficult to survive in a competitive environment. You may also run into adverse selection problems from both sides of the market. This focus will define your customer segment, distribution strategy, capital requirements, and product features.

Generally, if you are focused on improving access to a target market, you need to use some combination of unique data and a distribution advantage. As the company grows, the unique distribution channel(s) need to scale to serve that market. I think distribution is more important than data for a lending company. But if you are focused on reducing cost, it is important to be better than your competitors in reducing the cost of capital (financial engineering.) The target market already has access to a product (or a close substitute) and you are only providing it at a lower cost (sometimes with a better experience.) There is less room for charging a premium because the market is very price sensitive. It is difficult to compete long term on distribution or unique data.

Let’s take SoFi as an example — they are uniquely focused on lowering the costs for high-quality earners. Their borrowers have an average annual income of $150k, a monthly free cash flow of $5.7k, and an avg FICO of 756. The average income of $150k puts you in the top 10% of the US population. They have built the whole company around serving that customer segment and they don’t try to market to anyone who isn’t a part of that market. They can easily start offering loans at higher rates to more risky populations but they have no real advantage in terms of distribution or product (some would argue their community-based approach was differentiated but I disagree.) Their biggest advantage has been a lower cost of capital (which is needed to serve this highly coveted customer segment.) The founding team has a strong background in finance which was required to make the company successful.

This is how I view all consumer credit/lending startups:

If companies fall somewhere in the middle (or don’t choose a focus), they die quickly. They are not able to resonate with a target market, can’t distribute effectively, or compete with others in gaining mindshare. If there is a credit product for a certain segment of the market, the discovery is fairly efficient.

A similar thesis is now playing out for neobanks. Most of the up and coming neobanks are focused on improving access for a target population underserved by current financial services providers. It is imperative that they develop products to build deeper relationships with these customers (and charge a premium) instead of targeting the adjacent segment by reducing costs.

The market segments to improve access will eventually saturate but they are the best bet for a blue ocean for most B2C fintech startups.

A quick note on developing countries:

Developing countries are massively underpenetrated in terms of financial services. Consumers are hungry for any financial product they can get their hands on. Even a commodity product built for mobile will enjoy great success.

It’ll be interesting to see how quickly developing countries outpace the US in terms of the quality of financial innovation.

Hope this is helpful to new founders when building a fintech startup.

I wouldn’t have learned without help from a lot of people.

I am always around to help if you need any feedback or advice. Feel free to follow me or send me a note on twitter @rohitdotmittal.

Please subscribe if you liked it and would like to receive future essays.